When someone, for the first time, meets the word "Taxonomy," generally comes up against a wall, imagining a complex structure that only professionals of the sector can decipher.

Eu Taxonomy: the vocabulary of sustainability

When someone, for the first time, meets the word "Taxonomy," generally comes up against a wall, imagining a complex structure that only professionals of the sector can decipher.

Indeed, to a large extent, partly because of the name and mostly because of the complexity of this European Union legislation, this is the case.

On the other hand, the new EU guidelines give the opportunity to grasp simple aspects that are already present in the daily life and in the business of most people and economic activities, which are at the same time innovative, in order to step into and be guided in a new market: the sustainable finance.

The word Taxonomy, in fact, comes from the Greek word translatable into "tassinomia" and essentially means "to make order or give a classification."

Because this is what the European Commission, through a new regulation, aims to do: to establish a new language, new marco-classes, and a new common vocabulary or "Dictionary" is needed, therefore, first and foremost: establish a classification system that clarifies which investments are environmentally sustainable, preventing greenwashing and helping investors make greener choices.

Quite a challenge, then, when there is everything to be defined, including names or ground rules, especially when applied to a topic that is prioritized, not further postponed and even "creative," as may be that of "green" finance, or to use a less mainstream definition "ethical, sustainable finance with medium to long-term goals."

Herein arises the real question of the European Union that led to the development of the Taxonomy: how to combine the business and turnover aspects, on the finance and companies side, that also have to recover from a pandemic situation, with more qualitative aspects such as can be those of "ESG," that means “Environment, Social and Governance" characteristics?

Genealogy of Green Taxonomy

Since 2018 the European Union's first response has been channeled into the formation of an advisory table, the Teg "Technical Expert Group," made up of prominent people in the worlds of finance, law, business, and society, trying to figure out how to shape a new way of doing business.

In the first instance, not surprisingly, the Teg publishes in 2019 a kind of preview of the regulations, namely "The Non-Bunding Guidelines", where they give precisely "non-stringent" guidelines, to later develop the Taxonomy and decline it into the three areas: environment, social, and governance.

It should be noted initially that, as a primary approach, the Teg as an advisory member of the European Union, chooses not to sharply subdivide the three ESG areas of interest, but to connect them with a common thread, through a dynamic, science-based approach legislation that will over time establish legislation and standards to all three ESG pillars.

So far, it has seen the light and has been fully approved and legislated, the Taxonomy regarding the environment, published by the European Union in June 2020, including in itself in an embryonic way also some aspects of the Social Taxonomy, currently in the form of proposal.

Climate Targets: What the Taxonomy Regulation says

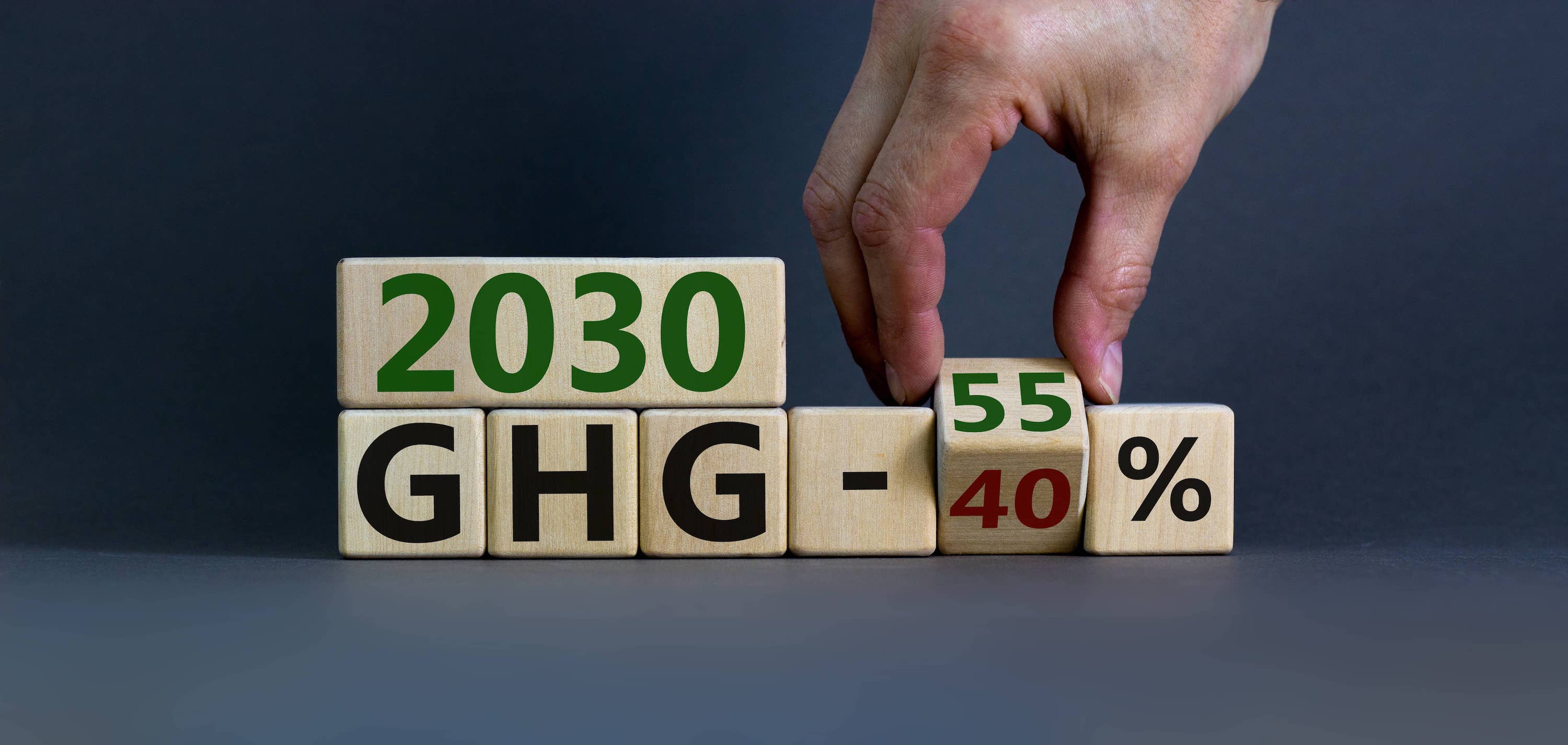

The EU Taxonomy, which essentially defines what a sustainable investment can be, in the part concerning the environment, first and foremost aims to regulate the thresholds for achieving the goals of the Paris Agreement (minus 55 percent emissions in 2030) and climate neutrality under the 2050 agenda.

To really do this, without too much "greenwashing," which translated means "talk to cover the facade of business aspects, mitigating them with ethical aspects of respect for the environment," a goal that the EU Taxonomy openly contrasts in the legislation, are established six key climate-related targets and the possible actions and ways that financial and non-financial companies can take to achieve them, measuring themselves with appropriate indicators, which for a target of about 50,000 companies will be mandatory from 2023.

The six objectives identified are, specifically:

- climate change mitigation;

- climate change adaptation;

- sustainable use of water resources;

- transition to a circular economy;

- pollution control and prevention;

- protection of a healthy ecosystem.

Of these so far the Taxonomy has declined, through appropriate Delegated Acts, the first two targets of climate change mitigation and adaptation.

By mitigation, the European Taxonomy legislation, means those actions undertaken by business activities, which manage to contribute substantially to the achievement of the thresholds set by the Paris Agreements, the SDGs and the Agenda 2050 and which already manage to redirect internal business activities in this direction, through low-carbon activities or enablers (i.e., which are about to undertake a business conversion in this direction).

Instead, by adaptation to climate change, the regulation means those business activities that, even if they do not contribute to emission reductions in economic activities, are able to adapt to climate change, through business strategies that allow for the stabilization and, thus, the non-rise of climate emissions.

In order to bring most European companies on board within this innovative system of conversion to environmental sustainability, the EU Taxonomy has introduced a third category, which thus affects the scope of economic activities involved in the ecological transition, defined as "transitional" and are the companies that adopt the conversion strategy that will involve most SME companies, starting in 2023.

The activities defined as transitional in the Taxonomy, in fact, stipulate that there is a focus on ethical sustainability issues, even if is still to be developed through innovative technologies and business, but which companies, through private and public investments are ready to undertake.

And here is the other key theme of Taxonomy: it is intended to serve as a compass, not only to channel investment from the EU or member states, but to attract also private investment and financial partners to support the sustainable change.

Indeed, the European Union, through this regulation and other related legislation, aims to be a leader in changing the world of finance and business, involving foreign countries and companies as much as possible, with one goal: to align the economy with ethics, with sustainability in all its components, through the filtering of ESG investment criteria.